The Infrastructure Is Real. The Timeline May Be the Bubble.

AI’s real risk is timeline misalignment: compute, power, capital, and enterprise adoption are scaling on different clocks.

Everyone wants to know whether AI is a bubble. The question is understandable, because the numbers are large enough that skepticism feels like basic financial hygiene. Goldman estimates roughly 1.6 trillion by 2031. The big four hyperscalers are on a roughly 81.6 billion in a single quarter.

It’s the wrong question.

In a normal bubble, people overestimate the value of the thing being built. A timeline bubble works differently: the thing may be genuinely valuable, but investors and operators assume the surrounding system will mature fast enough to capture that value on schedule. In many infrastructure cycles, the bubble lives not in the usefulness of the technology but in the timing, the financing, and the assumption that everything else will catch up fast enough. I have made a version of this mistake myself, more than once.

At EpiWatch, we spent years building a seizure detection algorithm. It worked: FDA-cleared, wearable, real-time. The kind of product where getting it right genuinely matters, because the alternative is someone having a seizure alone with no one coming. We achieved what we set out to achieve on the technical side earlier than most people would have expected, and then we discovered the algorithm was only the beginning.

To make the detection useful, you need a caregiver who trusts the alert, a physician who understands the product well enough to prescribe it, a patient who wears the watch consistently and keeps their phone nearby, and a support infrastructure that can handle the questions that come when something unexpected happens at 2am. The algorithm could fire perfectly and still fail to help anyone if any of those links were missing.

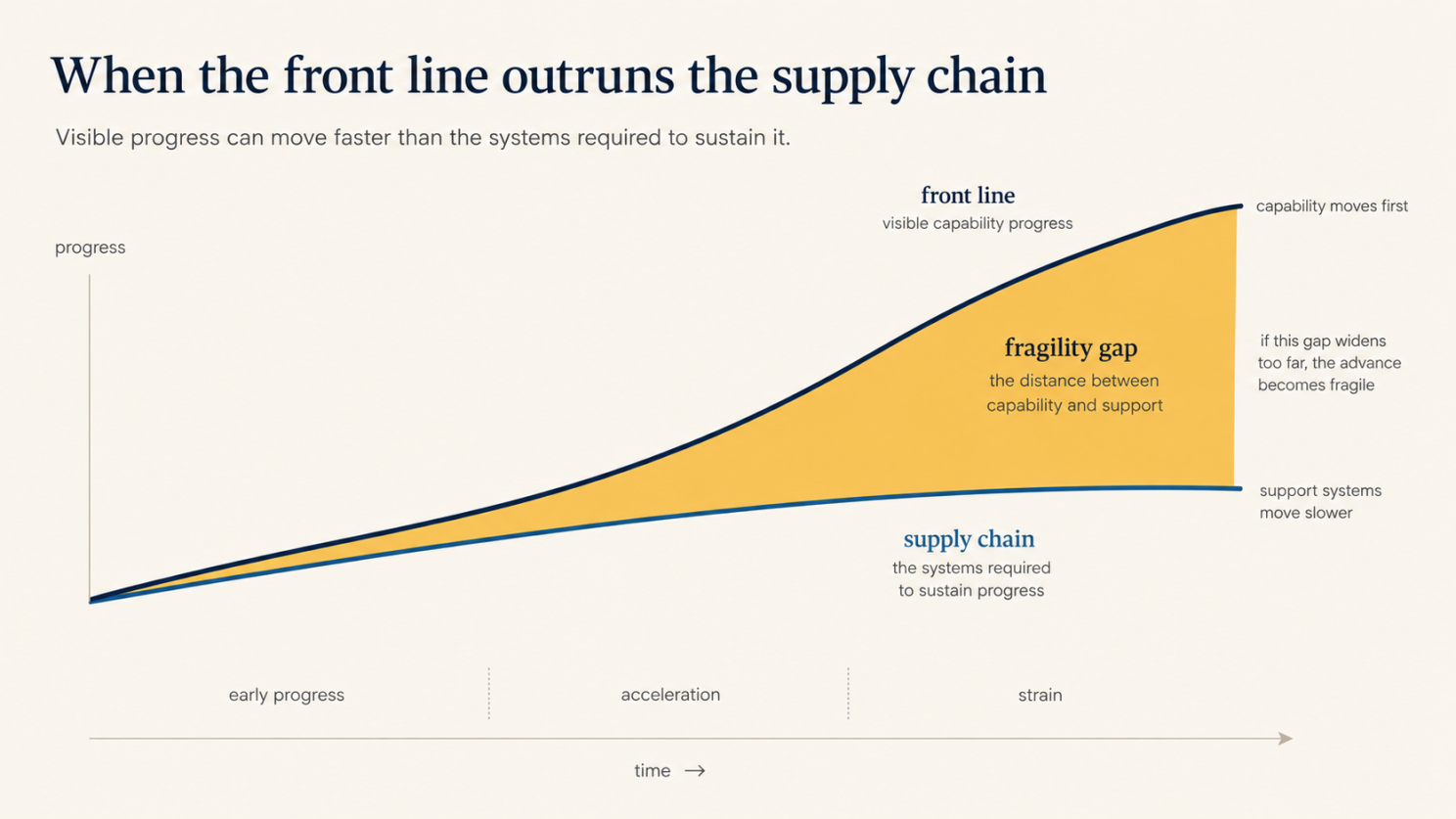

The technology was ready. The system around it needed time.

Move your forces too far ahead of your supply chain and you end up behind enemy territory with nothing to sustain you. Move too slowly and the war is decided before you arrive. The distance between your front line and your logistics it is the thing that determines whether the advance holds. At EpiWatch, the algorithm was the front line. Clinical infrastructure, patient understanding, caregiver trust, and prescriber familiarity was the supply chain. We moved the front line forward, but the supply chain took longer.

I have watched the same pattern play out in BCI. The science is doing things that look like science fiction (reading motor intent, restoring communication, interfacing directly with the nervous system), and the algorithms are extraordinary. But the clinical infrastructure, the reimbursement pathways, the trained specialists, the patient familiarity: none of that moves at the speed of a research breakthrough. The technology arrives. The world takes longer. I saw a commercial version of the same mistake at Orba, where we had a good product and a real market but underbuilt the distribution system around it: the customer definition, the market narrative, the repeatable path from interest to adoption. The surrounding system was the limiting factor.

This is the frame I keep returning to when people ask whether AI is a bubble.

The skeptics have real observations. Capital expenditure is growing faster than clearly attributable AI revenue, and enterprise adoption is widespread but uneven. McKinsey found that 88% of organizations use AI in at least one function, but only about one-third have begun scaling it enterprise-wide, and only 39% report EBIT impact. Deloitte found that just 34% of organizations are using AI to deeply transform core processes. There is a large difference between employees using AI and a company redesigning work in a way that produces durable economic returns.

A token consumed is not a workflow transformed.

At the infrastructure edge, though, demand signals are strong. Google Cloud backlog sits at $240 billion, Microsoft says Azure demand continues to exceed available capacity, and Amazon’s Bedrock processed more tokens in Q1 2026 than in all prior years combined. These are signals of genuine infrastructure demand. Both sides are seeing something real, just looking at different layers of the same system.

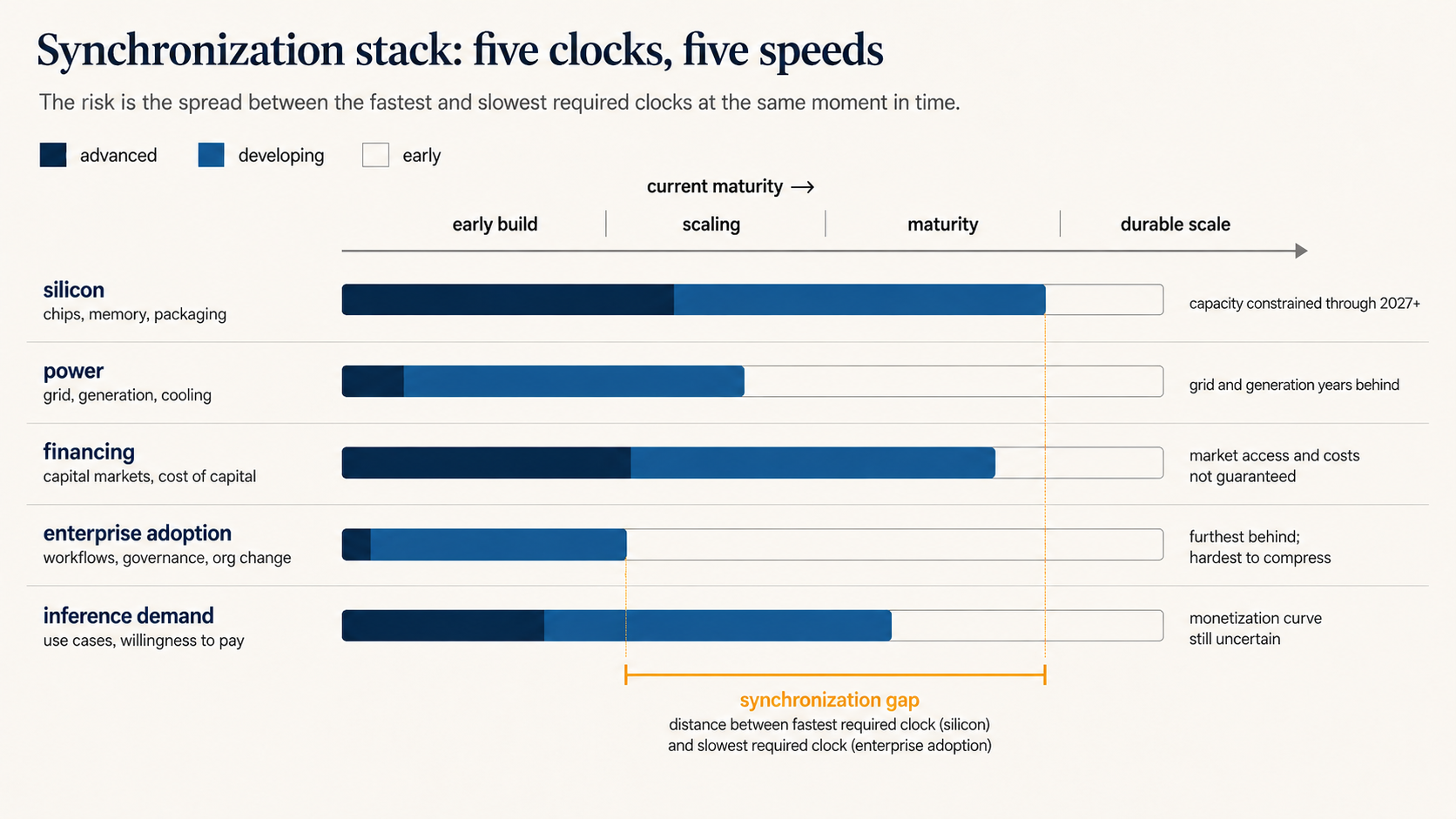

The better frame is synchronization. In AI infrastructure, the supply chain is not one thing. It is a stack of clocks: silicon, power, financing, enterprise adoption, and inference demand. The spending curve only works if those clocks mature on roughly compatible timelines. The synchronization gap is the AI version of the fragility gap, the distance between the fastest clock and the slowest one.

Silicon has to work. GPUs, custom ASICs, high-bandwidth memory, and advanced packaging need to arrive in sufficient quantity, at the right cost, and stay economically useful long enough to earn a return. HBM shortages are expected to persist through at least the end of 2027, a physical constraint with no software workaround.

Power has to work. Data centers need grid interconnections, transformers, transmission, cooling, and generation capacity. The IEA estimates that 20% of planned data center projects could face delays if grid risks go unaddressed, and global data center electricity demand is projected to nearly double by 2030. You cannot download a power grid.

Financing has to work. The hyperscalers are increasingly tapping debt markets to fund this buildout, with reports suggesting they may issue around $250 billion in public bonds in 2026 alone. That financing has to remain available at tolerable costs for long enough to matter.

Enterprise adoption has to work. Companies need to move from pilots and copilots to redesigned workflows, governance models, and production systems, and this is the clock furthest behind. Most large organizations have access to AI; what they have not built is the infrastructure around it: the governance, the accountability structures, the institutional knowledge of what good output actually looks like. The model may be ready, but organizational redesign does not ship on a schedule.

Falling inference costs expand the problem before they solve it. When machine cognition gets cheaper, companies use it in more places: agents, reasoning, video generation, compliance review, simulation, long-running background workflows. New workloads like video and agentic tasks can consume hundreds or thousands of times more energy per query than simple text generation. But absorbing cheaper cognition still requires permissions, data access, workflow redesign, security review, and people who know what to do with the outputs. The binding constraint may be decisions per organization.

Inference demand has to work. Reasoning, agents, video, coding, simulation, and robotics need to absorb capacity fast enough to justify the buildout before depreciation schedules catch up.

The risk is that five real things mature on incompatible timelines.

The top of the AI stack still looks like software (APIs, assistants, agents, enterprise platforms), but the bottom increasingly looks like utilities and project finance: capex, energy procurement, debt, depreciation, grid interconnection, power-purchase agreements, data center construction, asset utilization. Software investors expect high margins, low marginal costs, and asset-light scaling, but AI infrastructure raises different questions: how long do the assets last, what happens if model efficiency improves faster than expected, and who absorbs depreciation? Goldman views silicon useful life as one of the most influential variables in the infrastructure math. If accelerators become economically obsolete faster than accounting schedules assume, the return timeline deteriorates sharply. The useful life of a GPU may matter more to AI economics than the intelligence of the next model, and the real danger is owning utility-like assets while investors expect software-like returns. That asymmetry is where the timeline risk is concentrating.

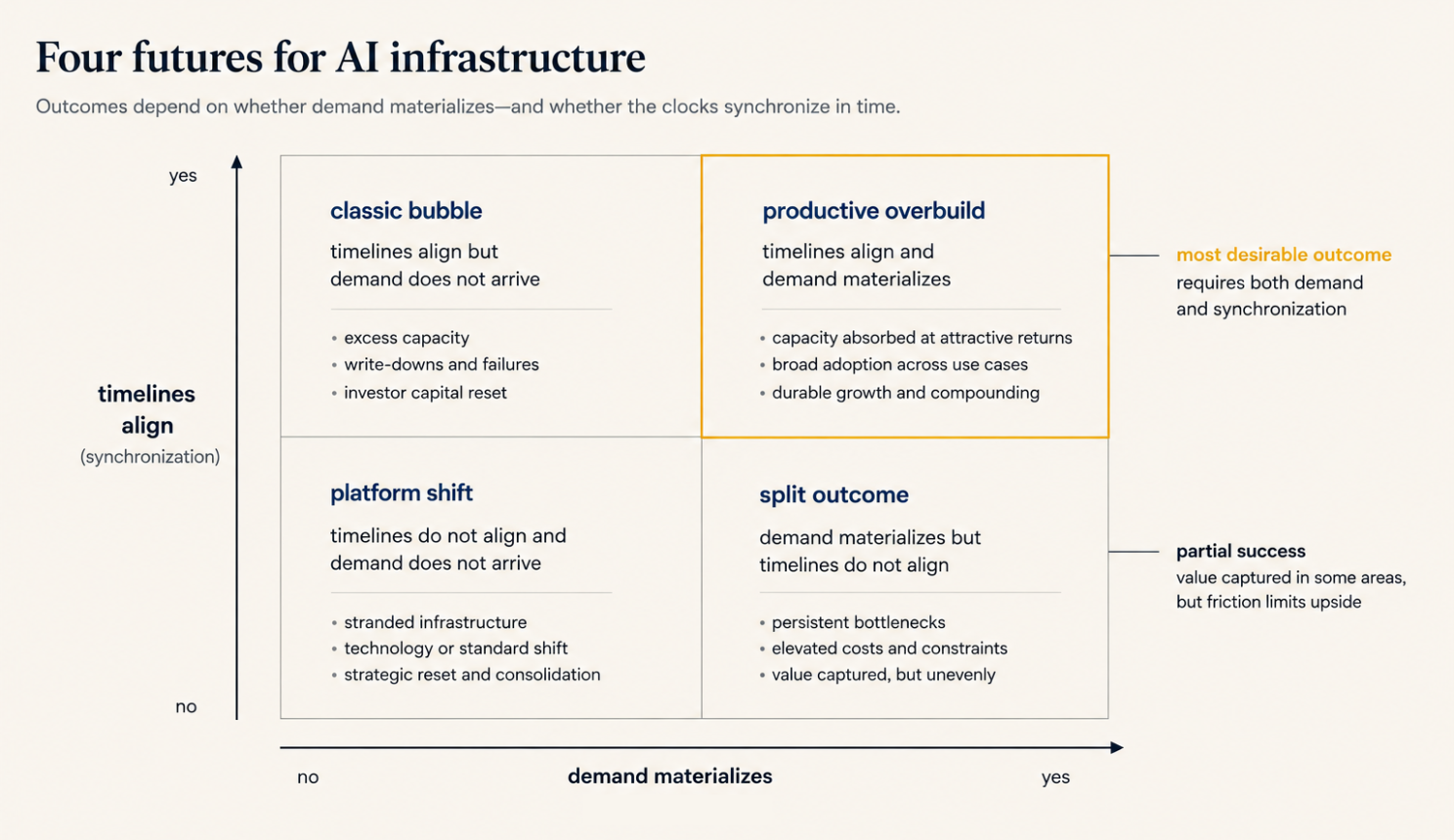

Mis-synchronization across layers has four possible endings.

If demand fails to materialize and financing tightens first, the result is the classic bubble. Spending outruns revenue, enterprise ROI disappoints, infrastructure sits underutilized, and depreciation rises faster than returns. The technology remains genuinely useful. Investors discover that useful and profitable at any price are different things.

If demand arrives but later than the capital assumed, the result is productive overbuild: the fiber story. Some capital is destroyed, and the infrastructure eventually gets absorbed by workloads that did not yet exist when the money was spent. This is painful for investors, but eventually useful for everyone else. The variable that determines which of those two it becomes is whether the financing structure survives the wait. Fiber companies went bankrupt, but the cable they laid did not.

If demand arrives fast enough and broadly enough, the spending looks aggressive in retrospect but rational. Reasoning, agents, video, robotics, and enterprise workflows absorb capacity faster than it can be built, and the infrastructure becomes the new cloud layer. This is the outcome the hyperscalers are currently priced for.

The fourth path is the one I think most likely, and worth arguing rather than asserting. The clocks synchronize, but unevenly. Demand materializes, but not for everyone. Some players own capacity and demand and distribution and the ability to shape where usage flows, while others own expensive undifferentiated infrastructure with no mechanism to influence utilization. The split outcome is the one the current structure of the market is predicting.

In AI infrastructure, owning the supply chain means owning the demand signal. Microsoft sees where enterprise usage is going because it deploys Copilot into the same workflows it sells Azure to run. Similarly, Google owns the surfaces where inference demand originates, and Amazon’s AI workloads arrive bundled with commercial relationships that predate the AI buildout entirely. Each of these companies has a structural claim on where demand lands, which means they can shape utilization in ways that pure infrastructure providers cannot. Everyone else is selling compute into a market those players are increasingly defining. Owning capacity proved necessary, but the verdict on the split outcome will be narrow and final: necessary was not sufficient.

There are a few indicators worth watching as this story unfolds. Revenue per watt of deployed capacity. Utilization rates in hyperscaler guidance. Whether enterprise AI spending is appearing in workflow redesign budgets or staying in the tools-and-pilots line. Bond spreads on data center debt, because that is where financing patience will first show signs of thinning. Perhaps most importantly, how many organizations have moved AI out of the innovation function and into operations. That is the enterprise adoption clock. It is the slowest one, and the spread between it and the silicon clock is where the timeline risk lives.

The infrastructure may be real. The timeline may be the bubble.